Build, Buy or Partner: Is change inevitable? (Part 1 of 2)

No change without a team. No change without cultural challenges.

In this post, I want to focus on the cultural challenges of such a change process. Why? Because corporate culture is, based on my 25+ years of experience, the essential make-or-break component. As we say: “Culture eats strategy for breakfast”.

But before discussing whether you should buy, form an allegiance or start a new business, it’s important to have a mutual understanding regarding the lifecycle-maturity degree of a. the incumbent and b. the innovation-centric startup.

On the one hand, we have a traditional bank that’s quite possibly been successful in the market for several decades making good revenue in its core business segment. The consensus there is that core business-related revenues and customers must be rigorously protected. Unavoidably, however, existing managers have become aware of ‘digitization’ and that customer behavior and preferences of interaction and transaction are changing. They can see this change on a daily basis simply by observing their kids’ digital activity. Then, first managers are using whats-app instead of email and visit fintech-conferences. Others follow. First ideas are discussed, facing first expected resistance. Central questions are: Why should we (re)act? What should be done? And then, of course: how to do it?

On the other hand, we have the fintech start-ups that are experts in e. g. digital customer-processing or at a specific product with expertise in segments of the B2B or B2C markets. Start-up industry realizes that incumbent players find it hard to act within that fast-moving innovative environment which is why they focus on that segment as future customers or exit-partners (many start-ups are tailor-made to potential exit-partners). That’s the match-making moment.

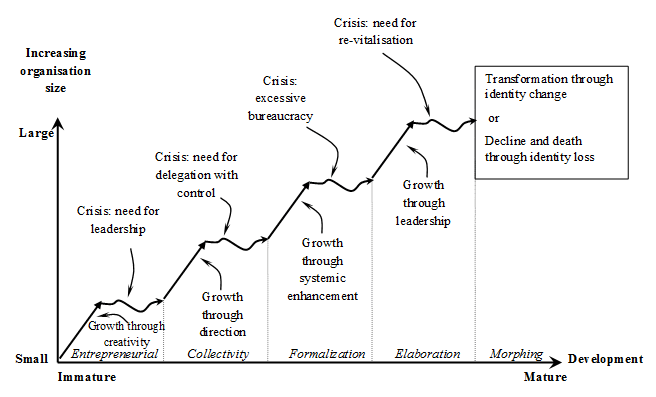

To understand what I’m aiming to get across, we now need to remember our university lectures and take a brief look back at the ‘Business life cycle’ model: By examining the maturity-degree of a company, we can assume the specific corporate culture. Then let us start to see why various conflicts could arise with each strategic option and why there can be no simple solution.

Figure 1: Pre-Configured Stages in the corporate life-cycle (adapted from Daft, 2008)

The above chart shows us that a traditional, established bank is in a pronounced ‘maturity’ stage of its life cycle. This bank has the opportunity to maintain its dominant position and grow with the industry. However, if the bank is not in a dominating position – something I would suggest is the reality for the vast majority of banks – then the bank needs to find a niche and defend it, or at least hold onto it. If none of these scenarios apply, the only inevitable strategic option left is a retreat. In the chart this is described as a ‘morphing phase’ involving a necessity for a change in identity – the alternative being decline and death.

I imagine traditional bank managers will not share this view. According to them, the business is running well, and they see no reason to worry. Profits won’t decline just because of a bit of digital ‘spin’. A phrase I’ve heard more than once at conferences is ‘We’ve been here for 150 years and we’ll always be here’. Firstly, I’d like to point out that 150 years does not equate to ‘always’. Secondly, research by Professor Richard Foster of Yale indicates that the lifetime of, for example, a listed company has drastically declined from 67 years in the 1920s to just 15 years today. And thirdly, we’re already in the midst of a movement towards consolidation: Incumbent banks are busy consolidating markets via M&A measures, and by that create a new company with a new “personality”, no matter what e. g. the brand itself might remain unchanged.

This brings us to the core of the matter: Nothing can be taken as granted, decision-makers at incumbent banks need to make some tough decisions. Banks have never been under so much pressure and at present, the entire business model is up for grabs. For the last years, decades, management teams have only focused on executing existing risk strategies. They’ve never had strong ownership for revenues, but high expertise in discussing cost-reductions. They have only rarely and selectively met with clients and have no experience with tough ‘real-world’ markets, having been solely involved with maintaining the status quo. (Analyzing your individual situation in your incumbent organization, I would be very happy if you could at least once disagree with my provocative description).

Out of a sudden, that management team now needs to question fundamental bank strategy and put themselves consequently in the spotlight. The result of that evaluation could indicate that action is or isn’t required.

If the latter is decided, we might call this ‘duck and cover’ (like in the last centuries 50ies, that “strategy” was the recommended behavior in case of a nuclear strike) in the hope that digitization will not have an impact. This may be down to a feeling that it’s possible to survive in a safe niche or a reassurance that customers will always need and use branches or simply avoid potential cannibalization –whatever the excuse might be for doing nothing. Taking this approach also has the advantage that no additional costs need to be incurred in the short term. Life can stay at its existing level of complexity. Great!

Alternatively, it could be concluded that action is required giving rise to a number of possibilities. In my next post, I’ll dive into possible strategies that banks could employ in order to meet the challenges faced by the banking industry today.

Spoiler alert: there is no ‘right’ answer

Related Articles

Jun 25, 2026

Modern Communications Surveillance in Financial Services: A Practical Guide to the Challenges and How to Get Ahead of Them

Jun 16, 2026

Shield Extends the Compliance Perimeter to AI-Generated Records and Image-Based Content

Subscribe to our newsletter

Gain access to exclusive insights, industry influencers, and thought leaders in

Digital Communications Governance and Archiving (DCGA).